The best teller at your bank might not be human. It’s an AI-powered assistant, working 24/7 as a hyper-efficient digital guide. These chatbots for banks are already here, handling thousands of customer queries at once, delivering instant service, and freeing up your human team for high-value work.

The New Digital Teller Is Already Here

Chatbots for Banks

Let’s face it: waiting on hold or rushing to a branch before it closes is a thing of the past. Customers now expect instant, personalized service on their devices, anytime, anywhere. This shift makes chatbots in banking a core business necessity for modern financial services, not just a tech novelty.

Think of a banking chatbot as your most effective employee. It operates around the clock on every customer’s smartphone, never gets tired, and handles countless tasks simultaneously. It can check balances for thousands, guide users through locking a lost card, and answer questions about transaction histories—all without human intervention.

Scaling Service, Driving Savings

This isn’t just about answering questions faster; it’s about transforming how banking services are delivered. By automating routine interactions, banks and credit unions are achieving massive operational gains. The cost savings are significant. Globally, financial institutions have been saving between $0.50 and $0.70 per interaction, which was projected to create $7.3 billion in annual operational savings by 2025. You can get more details on these AI chatbot statistics and their financial impact.

The real game-changer is scalability. A human agent handles one conversation at a time. A single chatbot manages tens of thousands, ensuring every customer gets an immediate response, even during peak hours.

This instant support improves the customer experience and, just as importantly, empowers your skilled financial advisors. Instead of resetting passwords, they can now focus on complex work that requires a human touch, such as:

- Providing in-depth mortgage advice.

- Assisting small business owners with financing.

- Resolving sensitive or high-stakes account issues.

To see the impact clearly, let’s compare banking before and after chatbots.

Chatbot Impact at a Glance

| Area of Impact | Traditional Banking | Chatbot-Powered Banking |

|---|---|---|

| Customer Service | Limited to business hours, with long wait times. | 24/7 instant support, no waiting. |

| Agent Focus | Repetitive tasks (password resets, balance checks). | Complex financial advice and relationship building. |

| Scalability | One agent per customer conversation. | One chatbot handles thousands of conversations simultaneously. |

| Cost Per Interaction | High, driven by human labor costs. | Extremely low, often under $1 per interaction. |

| Customer Access | Branch visits, phone calls, basic web forms. | On-demand service via mobile apps and messaging. |

This table makes it clear: chatbots don’t just add a feature; they transform the operating model of retail banking for the better.

More Than a Tool, A Strategic Shift

Integrating chatbots for banks is more than a tech upgrade; it’s a strategic pivot to a digital-first model. Banks that get this right aren’t just cutting costs—they’re building deeper relationships by being more accessible, responsive, and genuinely helpful.

These digital tellers are the new front line of modern banking. They meet customers where they are—on their phones in mobile banking apps and messaging platforms—providing the seamless, on-demand service everyone now expects. AI chatbots in banking leverage natural language processing and machine learning to understand queries, offer personalized guidance, and resolve issues instantly. Conversational AI is no longer optional; it’s a cornerstone of the AI banking industry in 2026.

This guide will show you how chatbots can also enhance customer experience, the tangible benefits they deliver, and how to deploy them effectively.

How Banks Deploy Chatbots in the Real World

Let’s move from theory to reality. Leading institutions, including Bank of America, are using chatbots to solve real problems and generate measurable value. These aren’t just glorified FAQs—they’re sophisticated tools integrated into the customer journey, transforming how banking gets done.

The numbers speak for themselves. The banking and finance sector leads in chatbot adoption at 83%, and an impressive 91% of banks with over $10 billion in assets now use AI chatbots for customer service. From handling routine transactions to providing insights through conversational AI, chatbots in banking are shaping the future of customer engagement.

Why? These bots automate up to 80% of routine inquiries, slashing call times and resolving issues on the first try. You can discover more insights about these chatbot statistics to see the full picture.

This is a strategic shift driven by applying AI to specific, high-impact areas for immediate results.

Automating Routine Customer Service

The most immediate win for banking chatbots is handling the constant flow of routine questions. These are the simple, predictable queries that used to jam phone lines and keep agents from addressing more complex issues.

A well-built chatbot handles these instantly, 24/7, offering a level of responsiveness that traditional call centers can’t match.

Practical Examples in Action:

- Balance Inquiries: A customer types, “What’s my checking balance?” and gets a secure, instant answer.

- Transaction History: “Show me my last 5 transactions” pulls the data directly from the core banking system.

- Card Management: A customer types, “Lock my card,” and the bot secures the account in seconds.

- Password Resets: The chatbot guides a user through a secure authentication flow to reset their online banking password, avoiding a lengthy phone call.

Customer: “I think I lost my credit card!”

Chatbot: “I can help with that. To keep your account safe, I can immediately place a temporary lock on your card ending in 4567. Should I proceed?”

Customer: “Yes please”

Chatbot: “Done. Your card is now locked. If you find it, you can unlock it right here. If it’s truly lost, I can help you order a replacement.”

Delivering Personalized Financial Insights

Modern banking chatbots do more than just react. They are becoming proactive financial assistants, using customer data to offer personalized advice that helps people manage their money better.

This transforms the chatbot from a simple support tool into a financial wellness partner.

By spotting patterns in spending, a bot can provide smart, helpful suggestions. This builds stronger relationships and shows the bank is invested in its customers’ financial health.

Examples of Personalized Insights:

- Spending Analysis: “You spent $250 on dining out this month, 20% more than usual. Want to set a budget for that category?”

- Subscription Alerts: “Heads up, we noticed a new recurring charge of $14.99. Should I add this to your tracked subscriptions?”

- Savings Recommendations: “You have $1,500 more than your average balance in checking. Moving it to savings could earn you an extra $5 this month. Want me to make that transfer?”

Generating and Qualifying Leads

Chatbots are also powerful engines for growth. The best banking chatbots act as an automated front line for finding and qualifying new customers. They engage website visitors and social media followers, identify their needs, and guide them to the right products.

By leveraging AI banking chatbots and agentic AI, banks can deliver personalized, real-time interactions while freeing up sales teams to focus on pre-qualified, high-intent prospects. This combination not only improves efficiency but also drives better conversion and customer satisfaction.

The chatbot does the initial legwork, asking the right questions before making a warm handoff. To see this in action, check out some of the best finance chatbots and how they work.

- Product Discovery: A chatbot greets a visitor with, “Are you looking for a personal loan, a mortgage, or a new credit card?” to guide them.

- Pre-Qualification: For a mortgage inquiry, the bot can ask for income and credit score range to offer an instant pre-qualification estimate.

- Appointment Setting: Once a lead is qualified, the bot can pull up a loan officer’s calendar and schedule a call automatically.

Simplifying Loan and Mortgage Processes

The loan and mortgage process is notoriously complex. Chatbots cut through that complexity by offering on-demand guidance, collecting initial documents, and providing real-time status updates.

This reduces friction for applicants and makes the workflow more efficient for the lending team. Instead of calling for an update, a customer can just ask the chatbot, creating a more transparent and modern experience.

Your Step-by-Step Implementation Roadmap

Rolling out a chatbot for your bank feels like a huge undertaking, but a phased approach makes it manageable. Start small, prove its value, and scale up from there.

This journey begins with strategy, not technology. Before you look at platforms, be clear on what you want the chatbot to accomplish. Are you trying to reduce call center volume? Generate more mortgage leads? Boost customer satisfaction? Without specific goals, you can’t measure success. Start by identifying your most frequent customer questions—these are your quick wins.

Phase 1: Define Goals and Select a Platform

Your initial goals must be concrete. “Improve service” is too vague. A better goal is “reduce routine balance inquiry calls by 25% within three months.” That’s a target you can track.

Once your goals are set, find the right technology partner. Not all chatbot platforms are ready for the strict demands of banking. You need a solution with:

- A No-Code Builder: An intuitive, drag-and-drop interface allows your business teams to build and tweak conversations without writing code.

- Bank-Grade Security: This is non-negotiable. The platform must offer end-to-end encryption and solid data protection to maintain compliance and trust.

- Integration Capabilities: Your chatbot must connect seamlessly with your core banking platform, CRM, and other software to pull real-time data.

A phased rollout is key. Start with one high-impact use case, like answering account balance questions. Once you prove its value, you can confidently expand into more complex areas.

Phase 2: Design, Train, and Integrate

With a platform selected, the design work begins. Map out the conversational flows—the step-by-step dialogues the bot will have with customers. The aim is to make these chats feel natural, helpful, and fast.

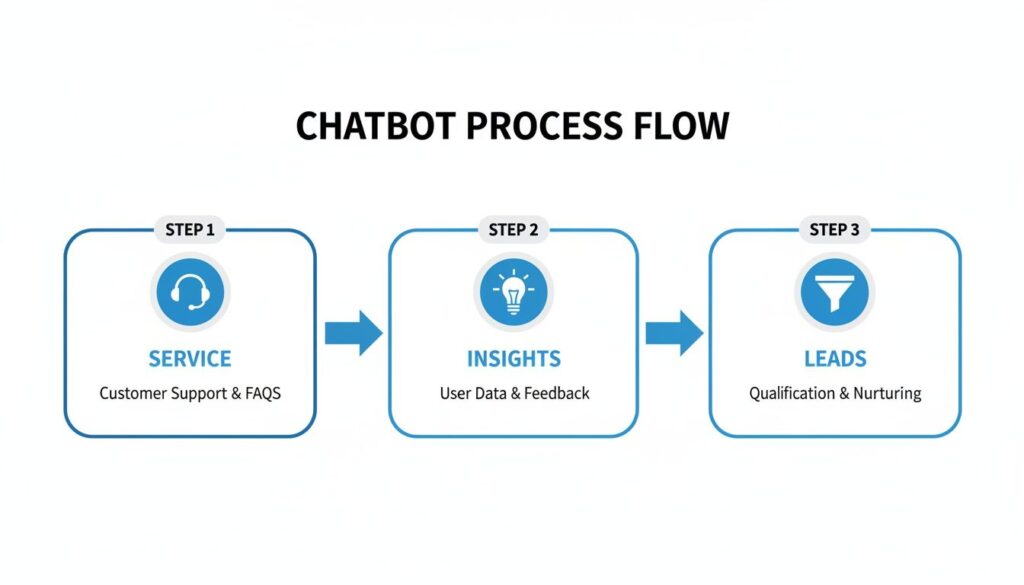

This infographic shows how a banking chatbot’s role evolves from basic service to a strategic tool for growth.

Chatbot for Banks Flow

A mature chatbot doesn’t just answer questions (Service). It offers proactive advice (Insights) and eventually drives business growth (Leads).

Next is training. Teach the AI all the different ways a customer might ask for the same thing. For example, “What’s my balance?”, “How much is in my checking?”, and “Show my account funds” all need to trigger the same action. The more variations it learns, the smarter it gets.

Finally, integration connects the chatbot to your live systems. This is what lets the bot fetch a real account balance or instantly lock a lost credit card.

Phase 3: Test, Launch, and Improve

Before a single customer interacts with your bot, your internal team needs to test it thoroughly. Push its logic, ask obscure questions, and verify every security protocol. This internal beta phase is your chance to fix problems before they impact customers.

Your initial “soft launch” should be targeted. Offer it to a small group of users or place it on a single webpage to monitor performance in a controlled environment.

Launching the chatbot is just the starting line. Continuous improvement is crucial. Watch these key metrics closely:

- Resolution Rate: What percentage of chats are successfully handled without a human?

- User Satisfaction: Are people rating their conversations well? Simple thumbs-up/thumbs-down feedback is valuable.

- Handoff Rate: How often does the bot need to escalate to a human agent?

Analyzing this data tells you where to focus your efforts. You can refine conversations, add new features, and make the chatbot more valuable over time.

Navigating Security and Compliance Challenges

Chatbots for Banks Digital Security

When it comes to people’s money, trust is everything. Bringing a chatbot into the mix raises valid questions about security and regulation. Your customers and your board need to know their data is locked down tight.

This isn’t just about ticking compliance boxes; it’s about proving your chatbot is a secure extension of the trust you’ve already built. Modern chatbots can actually make your bank more secure.

What Bank-Grade Security Means for a Chatbot

“Bank-grade security” isn’t just marketing fluff. It refers to a set of non-negotiable protections for financial data. For a chatbot, this means a multi-layered defense is baked in from the start.

Key Security Pillars Include:

- End-to-End Encryption (E2EE): This is your digital armor. From the moment a customer starts typing, the data is scrambled, like sending a message in a locked box that only the bank can open.

- Secure Authentication: The chatbot must work with your existing login methods, prompting for passwords, biometrics, or triggering multi-factor authentication (MFA) before showing account details.

- Secure Data Handling: Your chatbot should be a messenger, not a vault. It processes requests in real time without storing sensitive info like personally identifiable information (PII) in chat logs, minimizing risk.

This approach treats the chatbot as a secure gateway that verifies identity and pulls information from the core banking system, never becoming a vulnerable database of customer secrets.

Staying Compliant in a Regulated Industry

Banking chatbots must adhere to the rules of a heavily regulated industry. A well-designed bot doesn’t hinder compliance; it actively enforces it. Regulators are watching closely, as the CFPB issue spotlight addressing concerns about bank use of AI chatbots makes clear.

A huge advantage of chatbots is that every interaction is logged. This creates a perfect, auditable digital trail, making it far easier to run compliance checks than reviewing unrecorded phone calls.

Here’s how chatbots align with major regulations:

- GDPR: For banks with customers in Europe, chatbots must be designed with data privacy at their core, allowing users to request or delete their data.

- KYC and AML: Bots can assist with Know Your Customer (KYC) and Anti-Money Laundering (AML) efforts. They can be trained to flag suspicious language, monitor unusual requests, and escalate risks to a compliance officer. Getting this right involves understanding how customer identity resolution with AI creates a more secure ecosystem.

By automating and documenting interactions, a chatbot helps create a more transparent and secure environment, addressing regulatory concerns while building deeper trust with customers.

How to Measure Chatbot Success and ROI

If you can’t measure your chatbot, you can’t prove its worth. To justify the investment and show a real impact on the bank’s bottom line, you have to track what truly matters.

You’re not alone. 73% of banks globally have deployed at least one chatbot, handling billions of interactions monthly. More importantly, customer satisfaction with these bots is hitting a remarkable 84%, proving they deliver when done right. You can see a full breakdown of these banking chatbot adoption statistics to understand the industry’s progress.

Key Performance Indicators for Banking Chatbots

How do you measure success? It’s not about one magic number. A clear picture emerges when you track a balanced set of metrics across three areas: cost savings, customer happiness, and business growth.

This table breaks down the most important Key Performance Indicators (KPIs) to watch.

| Metric Category | KPI | What It Measures |

|---|---|---|

| Operational Efficiency | Resolution Rate | The percentage of conversations fully resolved by the chatbot without human intervention. |

| Operational Efficiency | Cost Per Interaction | The total chatbot-related costs divided by the number of conversations, showing direct savings. |

| Customer Experience | Customer Satisfaction (CSAT) | User-reported satisfaction scores, typically gathered with a simple post-chat survey. |

| Customer Experience | User Retention Rate | The percentage of users who return to use the chatbot for subsequent inquiries. |

| Business Growth | Leads Generated | The number of qualified leads (e.g., loan applications, new account sign-ups) initiated by the bot. |

| Business Growth | Product Upsell Rate | The percentage of interactions where the chatbot successfully cross-sells or upsells a product. |

Tracking these KPIs together provides a complete view of your chatbot’s performance, ensuring you’re not just cutting costs but also delighting customers and growing the business.

Calculating Operational Efficiency

These are the metrics your CFO will love. Operational KPIs provide a direct, dollars-and-cents view of how your chatbot saves the bank time and money.

- Resolution Rate: Your number one metric for bot effectiveness. A high resolution rate—ideally 80% or more for common questions—proves the chatbot understands and solves customer problems on its own.

- Containment Rate: Measures how many conversations start and end with the bot, without needing a human handoff.

- Cost Per Interaction: Here’s where the ROI shines. If a human-led call costs $8 and a chatbot interaction costs just $0.65, every resolved issue represents a clear saving of $7.35.

Measuring the Customer Experience

Saving money is great, but not if it drives customers away. Experience metrics are your guardrails, ensuring efficiency doesn’t sacrifice customer loyalty.

Customer Satisfaction (CSAT) is your north star metric. A simple “Was this helpful? 👍/👎” at the end of a chat provides instant, actionable feedback.

To monitor customer experience, focus on:

- Customer Satisfaction (CSAT): Aim for 80% or higher. Low scores tied to a specific topic, like “check fraud,” give you a clear signal on where to improve.

- User Retention Rate: Are people coming back? A high retention rate shows customers found the bot genuinely helpful.

- Average Handle Time (AHT): How fast does the bot solve the problem? A low AHT means a quick, frictionless experience for your customer.

Proving Business Growth and Calculating ROI

This is where your chatbot becomes a revenue-generating asset. The goal is to directly tie the bot’s activity to business growth, building a case for further investment.

For instance, if your chatbot pre-qualifies 100 mortgage leads in a month and 10% become approved loans, you can directly attribute that new business to the bot. That’s a powerful story.

A simple ROI formula to get started is:

ROI (%) = [ (Total Savings + New Revenue from Chatbot) – Chatbot Investment Cost ] / Chatbot Investment Cost * 100

By consistently tracking these KPIs, the conversation shifts from “Does our chatbot work?” to “How can we empower it to do even more?” This numbers-first approach is key to demonstrating measurable success.

Choosing the Right Chatbot Platform

Picking a chatbot platform is a major strategic decision. In the high-stakes world of banking, your tech partner directly impacts your security, customer trust, and bottom line. A generic, off-the-shelf bot won’t cut it.

Think of it as hiring a new team member who will talk to thousands of your customers daily. You wouldn’t skip the background check. The right platform is a solid foundation for building secure, helpful chatbots for banks. The wrong one is a fast track to security holes and customer frustration.

Your Must-Have Feature Checklist

When evaluating vendors, you need a checklist built for financial institutions. You’re looking for enterprise-grade muscle designed for the unique pressures of banking.

Here are the non-negotiables your platform must deliver:

-

Robust Security and Compliance: This is ground zero. Your vendor needs proven security credentials like SOC 2 and ISO 27001 certifications. Demand end-to-end encryption, secure data protocols, and a clean way to plug into your bank’s existing authentication, including multi-factor authentication (MFA). No compromises.

-

Seamless Core System Integration: A chatbot that can’t talk to your core banking system is just a glorified FAQ page. Your platform must have powerful API capabilities to connect with your core, CRM, and other critical software. This turns a simple Q&A bot into a tool that can check a balance or lock a card in real time.

-

A User-Friendly Conversation Builder: Your business teams should be able to design and tweak conversations without needing a developer for every change. A no-code, drag-and-drop interface is essential for agility, allowing you to launch new flows and react to market shifts without a six-month IT project.

Beyond the Basics: Strategic Capabilities

Once you’ve nailed the essentials, look for features that separate a simple tool from a true strategic partner. These are the capabilities that let your chatbot program grow and deliver more value over time.

Choosing a vendor is about more than just software; it’s about finding a partner that understands the financial industry. They should provide expert support and strategic guidance, helping you navigate compliance and scale your automation efforts.

Look for these advanced functions:

-

Multi-Channel Support: Your customers are on your mobile app, Messenger, and WhatsApp. The platform must support all these channels from a unified backend for a consistent experience everywhere.

-

Intelligent Human Handoff: No chatbot can solve everything. When a customer needs a person, the handoff must be seamless. The platform must transfer the entire conversation history to the live agent, so the customer never has to repeat themselves.

-

Advanced Analytics and Reporting: “What you can’t measure, you can’t improve.” You need a dashboard with a clear view of metrics like resolution rate, customer satisfaction (CSAT), and containment rate. This data proves your ROI and shows you where to focus improvement efforts.

For a deeper dive into the features that make a chatbot solution truly enterprise-ready, check out our ultimate guide to enterprise chatbots.

By prioritizing these features, you’ll choose a platform that not only solves today’s problems but also grows with your bank’s digital ambitions for years to come.

Your Top Questions About Banking Chatbots, Answered

As banking chatbots become more common, it’s natural to have questions. You might wonder how they’re built, what they can really do, and most importantly, if they’re safe. Let’s tackle the big questions head-on.

Ready to see how a secure, intelligent chatbot can transform your customer engagement? With Clepher, you can design, build, and deploy powerful AI chatbots using an intuitive no-code builder. Start automating service, generating leads, and delivering personalized banking experiences on your website, Messenger, and WhatsApp today.

Related Posts

Chatbots for Banks: The Ultimate Guide for 2026

April 4, 2026Mastering Conversational AI for E-commerce Success

April 3, 2026Turn Visitors Into Leads With a Web Chat Widget

April 2, 2026

Founder Clepher